Although every organization defines it a little differently, overhead is a generic term for the cost of doing business. These typically include: indirect costs, administrative costs, shared costs and fixed costs, although depending on the organization, they can also include the salaries and expenses for everyone who is not providing program services.

Overhead isn’t an accounting term but it gets used regularly in businesses, nonprofit and otherwise. The purpose of this newsletter is to help NPOs to agree on how the term will be used in your organization, to:

- Be fiscally responsible;

- Adequately fund the organization’s mission, and

- Maximize the organization’s sustainability.

A definition to begin the conversation: The table below classifies various functional expenses of a nonprofit, all of which are reported on an IRS Form 990. Administration and fundraising are typically part of overhead expenses.

Functional classification of expenses *

| Function | Definition | Examples |

| Program | Expenses related specifically to carrying out your-mission-related work | Salaries and benefits of program staff, program supplies and the portion of occupancy costs incurred by program activities |

| Administration | Expenses not related to program or fundraising but that are essential to the organization’s operation | Salaries and benefits of finance staff, a portion of the executive director’s salary and benefits, board-related costs, and the portion of occupancy costs incurred by administrative staff |

| Fundraising | Expenses related to soliciting contributions for the organization | A portion of the salary and benefits of any staff who participate in grant writing, special events, cultivation and solicitation of individual or corporate donors, and the portion of occupancy costs incurred by fundraising staff |

Table drawn from FINANCIAL LEADERSHIP FOR NONPROFIT EXECUTIVES: Bell, J & Schaffer, E. a Compass-Point-Fieldstone Alliance Book (2005)

BE FISCALLY RESPONSIBLE:

Key to fiscal responsibility are:

(a) Ensuring that you have someone who understands the rudiments of accounting and

(b) Leadership willingness to talk openly, honestly and effectively with donors and your board about the costs of doing your organization’s business and why it is actually a good thing to raise money, hire qualified staff, and run an effective and efficient business.

It’s important to do your homework and not rely solely on the accountants. Not only does organizational staff need to be clear and transparent about reporting programmatic, administrative and fundraising costs, they need to be savvy about how to do so. For example, if an Executive Director (ED) makes the time to do 2-week biannual time tracking, this sample will provide a better picture for the Board, the public and the IRS of what ED and/or program staff really do with their time rather than lumping time into a generic classification of “management and general”, essentially making them part of overhead. Instead, a closer look at the ED’s time might show that 70% of her time is spent on program, 20% on management and 10% on fundraising. This evidence can be used to allocate the ED’s time across program and funding categories, as well as administration, and will be useful in conversations with the board about how many staff are needed to adequately address the organization’s mission, whether additional staff are needed and whether their time should be allocated for program, fundraising, or other activities.

Talk with your accountant about how to define “overhead” in your organization and make sure you understand:

- Classification of expenses ( see chart above)

- How employee and ED time is tracked.

- Allocation of common costs, :

- Treatment of restricted and unrestricted contributions

- Use of accrual based accounting to ensure that earned revenue is matched with related expenses

- Capitalization and depreciation, to spread the costs of capital acquisitions, their use and estimated useful life across multiple years. Capital expenses: (equipment) show up as an asset on the balance sheet, but not in the income/expense statement. Their depreciation is an overhead expense, required by accounting rules

FULLY FUND THE CORE MISSION:

Why do we get into trouble talking with donors and our boards about how much it costs to fund the mission? The short answer is: a lack of understanding about the real costs of doing business and uncertainty about how to report overhead correctly. Historically, Boards and donors have looked at financial ratios (cost of program outcomes versus administrative and fundraising costs) as a measure of organizational effectiveness. Approaching nonprofit finance in this way leads to misrepresentation of both processes and outcomes. In a “Nonprofit Starvation Cycle” https://ssir.org/articles/entry/the_nonprofit_starvation_cycle), the Stanford authors describe how the overhead myth and nonprofit starvation cycle have led to a spiral of nonprofit underinvestment in core costs and a lack of transparency about what is needed financially to realize nonprofits’ missions.

In response to this article, the Presidents/ CEOs of the Better Business Bureau Wise Giving Alliance, GuideStar USA and Charity Navigator have formed a coalition to help end the “Overhead Myth”. In a joint statement issued in 2014, they asked nonprofits to join them in re-envisioning how nonprofits describe their core mission costs, including fundraising and administration. They ask that we commit to this re-envisioning by:

- Demonstrating ethical practice and sharing data about organizational performance.

- Proactively sharing information about goals, strategies, and management system so donors will trust us.

- Understanding the true costs of achieving our mission and managing toward those results, and

- Educating funders (individuals, foundations, corporations and the government) on the real cost of our program outcomes.

Information about how to participate in this initiative is available at: www.overheadmyth.com

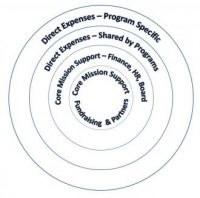

Here is a re-envisioning example: We have historically used a pie-chart to describe our organization’s financing. Perhaps we report 60% of our budget as “program costs”, with the remainder divided between administrations and fundraising. This underfunds what we financially need to accomplish the mission.

Instead, we need to think about our investment in key infrastructure as part of our core mission support. Core mission support includes: financial, human resource and Board support. Core mission support also supports funding raising and work with our partners. In addition, we have program specific direct expenses and expenses shared by programs. These graphics can be found at www.propelnonprofits.org/blog/a-graphic-re-visioning-of-nonprofit-overhead/ and used to describe this approach to your board or staff.

Instead, we need to think about our investment in key infrastructure as part of our core mission support. Core mission support includes: financial, human resource and Board support. Core mission support also supports funding raising and work with our partners. In addition, we have program specific direct expenses and expenses shared by programs. These graphics can be found at www.propelnonprofits.org/blog/a-graphic-re-visioning-of-nonprofit-overhead/ and used to describe this approach to your board or staff.

MAXIMIZE YOUR ORGANIZATION’S SUSTAINABILITY:

We need to honestly fund our nonprofits for both their everyday programs and their overhead expenses. Doing so, will give nonprofits some fiscal flexibility. As a result, they can better plan and execute program services within their organizational niche. Nonprofits also need to generate fiscal surpluses to reinvest in the organization’s immediate and future health. After paying operating expenses, surplus resources are important to:

- Meet unexpected liquidity needs – paying the bills on time

- Protect against risks and take advantage of new opportunities

- Add to fixed assets and

- Make principal repayments on debt.

Funding these full costs and adopting new ways to talk about overhead will contribute to your sustainability and further the dialogue to end the overhead myth. For more information and resources on covering full costs see Claire Knowlton’s January, 2016 article in the Nonprofit Quarterly: https://nonprofitquarterly.org/2016/01/25/why-funding-overhead-is-not-the-real-issuethe-case-to-cover-fill-costs/